How to Open a Company in Portugal

Essential Steps for Foreigners

Overview

Portugal is an increasingly attractive jurisdiction for foreign investors, offering a flexible corporate framework. Foreign individuals and entities are free to incorporate companies in Portugal, provided that the applicable legal requirements are met.

This note outlines, in a practical and structured manner, the key legal steps involved in establishing a company in Portugal.

Step 1 – Tax Identification (NIF/NIPC)

Prior to incorporation:

• All individual shareholders and director must obtain a Portuguese Tax Identification Number (NIF)

• Where a shareholder is a foreign legal entity, a Portuguese equivalent entity number (NIPC) must be obtained in advance.

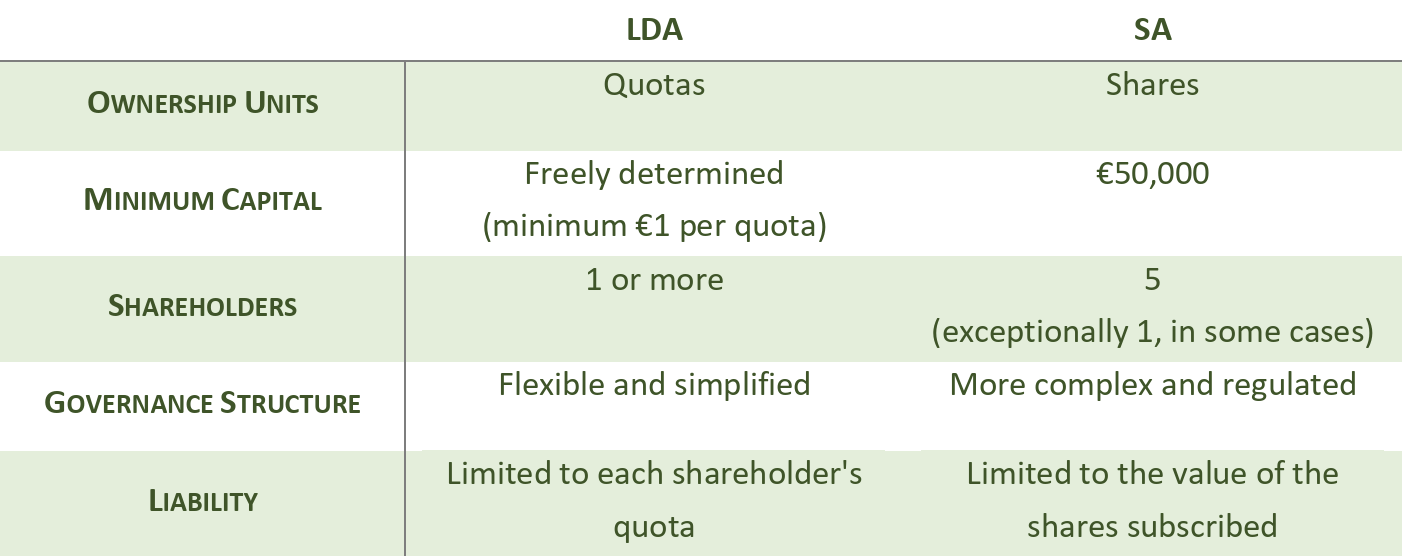

Step 2 – Choosing the Legal Form

The two corporate structures most frequently adopted by foreign investors are:

▪ Private Limited Liability Company (LDA) – most commonly used structure, particularly for SMEs

▪ Public Limited Liability Company (SA) – tipically adopted for large businesses and investors

Step 3 – Defining the Corporate Structure

Prior to incorporation, several structural elements must be determined:

1. Company name

- One of the following options may be used:

▪ Request a certificate of admissibility for up to 3 proposed company names

▪ Select a pre-approved name from the official list

▪ Use a combination of shareholder(s) name(s)

- The company must include the mandatory legal designation “Lda.”, “Unipessoal, Lda.” or “S.A.”

2. Registered office in Portugal

3. Corporate purpose

- Defines the scope of activities the company intends to pursue. It should be drafted with sufficient breadth to allow commercial flexibility, while remaining consistent with the intended business model

4. Share capital and allocation among shareholders

- Should reflect the economic reality of the investment and the intended allocation of control

- Shareholders are free to determine the capital structure

- No maximum number of shareholders

- Contributions may be made in cash or, subject to legal requirements, in kind o Limited liability

5. Management structure

- The company must formally appoint its management body:

▪ In a LDA, management is entrusted to one or more managers

▪ In a SA, management is tipically exercised by a Board of Directors, although a single director structure may be adopted in certain cases

- Managers or directors may be shareholders or third parties

Step 4 – Incorporation and Registration

Incorporation is formalised through registration with the Commercial Registry, either by adopting standard articles of association or by executing customised articles of association.

Upon registration:

- The company acquires legal personality

- A corporate tax number is issued

- The company becomes legally capable of conducting business

Step 5 – Bank Account & PTA

Following incorporation:

- A business bank account must be opened in Portugal

- Share capital must be deposited

- Within 15 days, the company must declare the commencement of activity before the Portuguese Tax Authorities.

Ongoing accounting and reporting obligations apply under Portuguese law.

Common Questions (Q&A)

Can a company be incorporated with a single shareholder?

Yes. Portuguese law expressly permits single-shareholder companies. However, (i) a natural person may not be the sole shareholders of more than one single-member LDA, and (ii) a single-member company may not be the sole shareholders of another single-member company

Is Portuguese residency required?

No. Shareholders and directores are not required to reside in Portugal.

Must shareholders hold equal participation?

No. Participation percentages are freely determined by the shareholders.

Can quotas/shares be freely transferred?

Yes. However:

- In a LDA, the transfer to third parties requires the approval of the company, unless the articles of association provide otherwise.

- In a SA, share are freely transferable, unless restricted by statutes.

Can the company’s share capital, corporate purpose or name be amended after incorporation?

Yes. Following incorporation, the company may, at any time, amend its key elements, including its share capital, corporate purpose and company name. Sucha amendments require registration with the Commercial Registry.

Is the company required to prepare annual accounts?

Yes. Portuguese companies are required to appoint a certified accountant responsible for tax compliance and accounting obligations.

Is the company required to prepare annual accounts?

Yes. All companies must:

- Maintain organized accounting records;

- Prepare annual financial statements

- Approve and submit annual accounts

Failure to comply may result in fines and restrictions on certain corporate acts.

This Informative Note is intended for general distribution to clients and the information contained herein is provided as a general and abstract overview. The contents of this Informative Note may not be reproduced, in whole or in part, without the express consent of the author. If you should require further information on this topic, please contact us at info@reispintolaw.com.